If you’re not coming from one of the more affluent member states, getting a job in an EU institution can make you elated. Also because of the expected higher income and other benefits.

However, it’s best to be financially cautious at least for the first few months of your job and do some financial planning beforehand. Otherwise, you might experience cash flow headaches instead of the positive thrill of a new job and meeting your diverse bunch of colleagues from all over Europe.

Why the caution?

Reason 1: extra costs

Settling in in a different country, or even a different city in your own country comes with extra costs. These can be:

- Increased costs because you’re in a country’s capital or because locals charge extra for expats, or you don’t know how to find deals.

- Safety deposit, at least a month’s advance pay for apartment rental, plus one-time agent’s fee. In some countries you have to provide up to three monthly rent payments at the start of the rental contract.

- Need for new clothing if your EU job is more formal than the last one.

- Furniture, especially if the apartment is non- or partially furnished.

- If you have kids, kindergarten and school enrolment costs and regular fees.

- Relocation costs. You’ll get transportation costs fully/partially reimbursed with your 2nd month’s salary, however these can be substantial.

This expenditure is often coupled with at least a temporary loss of your spouse’s income, if you happen to have a partner and she/he moves with you.

In other words, if you’re not careful and don’t have savings, you might be looking at a cash flow challenge in your budget for around two to six months, depending on the particularities of the country and your personal habits and lifestyle demands and aspirations.

Reason 2: EU salary payment rules

You might get your first salary after two months

Most people assume that as of the first month they will get the full EU salary with all the allowances and other payments. This is usually not the case.

EU institutions advise to plan that you will get your first salary payment after two months of working. This because it takes a lot of paperwork to enter the records of a new EU employee in the various systems. However, you’ll get both first and second months’ salaries in one payment.

There are some EU institutions that are more “user friendly”. However, the best they can offer is to pay your ‘basic salary’ in the first month, i.e., salary without any of the allowances. If you do not have any savings to rely on, request an advance salary payment as soon as you arrive to the HR department.

You most definitely do not get even the basic salary payment if you arrive at your new post in the middle of a month (institutions let new hires start on the 1st or the 16th of every month). To get your first salary, you’ll have to wait until the 15th of the next month, however, then you’ll be paid the 2nd month’s basic salary plus the proportional part of the 1st month’s salary. If you get lucky, you might already be paid all the allowances in the 2nd month, but don’t assume it to be guaranteed, and file all the paperwork immediately.

Always consult with HR in detail and make friends with a more experienced colleague that can help you to understand the system and whom to contact to facilitate things.

Why don’t the EU institutions pay a full salary in the first month?

You will not get the full salary in the first month becasue it has to do with the fact that the HR unit and the PMO or the EU’s Paymasters Office have to ‘determine entitlements’. Your final salary is impacted by a number of factors that the institutions can check only once you’re employed, aka, your original employment and education documentation, your work experience length, whether you’re an expat, whether you have kids, whether they have relocated with you, is your spouse with you, what’s her income, etc. This objectively takes time.

It is in your own interests to fill any forms and provide any information requested by HR or the PMO ASAP. The faster you do this, the more likely is your chance to get a full salary in the 2nd month of employment.

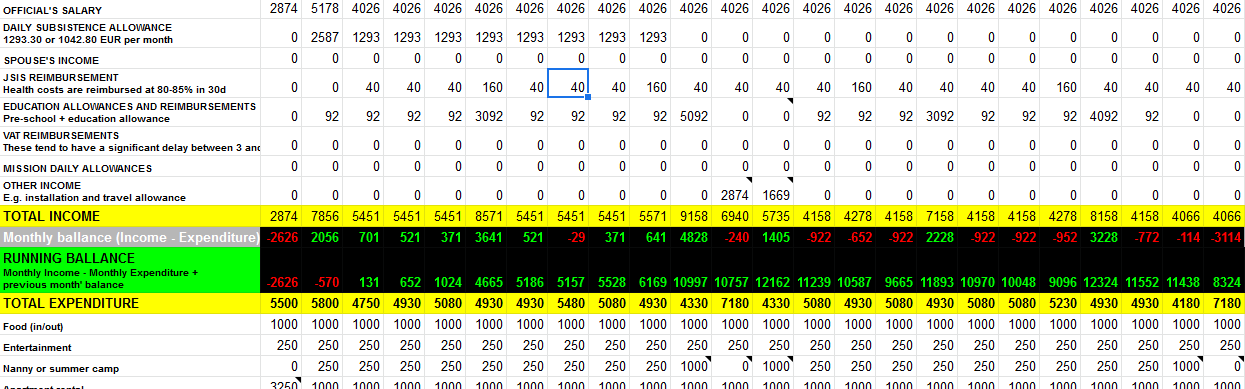

Sample calculation of your cash flow challenge

Let’s assume that you are a new employee of the EU satellites agency in the Czech Republic where the correction coefficient of 0.83 or 83% of a Brussels salary applies. You successfully got a three-year contract agent’s position of FGIV and are starting at grade 13 step 1.

You do not have any mortgage or other loan payments before getting the EU job and you and your family agree to live relatively frugally, however splurge once a year on a holiday abroad. You have a spouse that won’t work at first (and might never find work in Prague) and two kids – one in pre-school and one that is school-aged. You also will rent a two/three bedroom 80m2 apartment for around 1000 EUR a month and start to make monthly payments for a car you bought a few months in to your new job.

Below is a simulation of what your budget and cashflow might look like. Open the picture in a new window or take a look at the link below the picture.

Feel free to download or copy the sample budget to play around or even use as your own budget planning tool.

I would assume that most families spend more than in the sample budget (for example, on Christmas or the annual holidays), so adjust the numbers to your particular situation. Remember to add any existing liabilities like a property mortgage, any car loan, credit card debt, as well as additinal income, i.e., if you have rented out the apartment back home.

Things to pay attention to

- Start of the contract is not the only time when you might experience cash flow problems.

- Be aware that the Daily Subsistence Allowance will stop after either the 4th or the 10th month decreasing your income by around 1000 euros monthly. Don’t get used to it and better save it up.

- Pay attention to the terms and conditions of your kids’ school costs reimbursement rules. If the location of your institution does not have a European School, you might have to regulary for 3 to 5 months of school costs that are reimbursed retroactively.

- Bigger expenses might throw your financial planning off balance like the annual holiday or buying a car.

In other words, even if you get a higher salary in our EU institution compared to the one back home, try to stick to your former lifestyle for at least the first year to evaluate if you can afford any “upgrades” or “lifestyle creep”.

While EU jobs often come with additional income, life in a different country usually also comes with additional expenses.

Tips to make the cash flow pressure easier on your budget

01 | Strategically timed relocation

- If you have a family, move alone for the first two months. This way your spouse can continue working and you can more easily prepare everything for the family’s arrival. You also might not have enough money for all the payments associated with your family’s arrival like a security deposit for an apparment and buying furniture.

- Consider a short-term rental in the first month or two. This not only lets you get acquainted with the city, but also removes pressure to rent the first available long-term rental. It also allows to manage costs as you won’t have to pay rent for a family-size apartment/house and won’t incur a safety deposit and agent’s fees just yet. Lot’s of expats go for AirBnB’s as they are cheaper than hotels and offer more comfort. If you never rented through AirBnB, please register here (an affiliate link – you’ll support this blog at no extra cost to your wallet).

02 | Pre-school and school costs

- If you have kids, you are entitled to a pre-school and an education allowance, however, it’s not possible to arrange these in the first month of arrival. Having your family arrive a month later or even after that allows you to get all the documentation in order. I have a separate article about this.

- If the school you’ve chosen expects you to sign a contract right away, try to negotiate a full or partial delay school of (entry and regular) fees for the first few months. It never hurts to ask and many schools are forthcoming. Additionally, many institutions offer stuff to provide explanatory or assurance letters assuring schools that you’re a financially solvent parent just settling in a new country.

- Besides the EU pre-school and education allowances, you might be entitled to additional education-related financial assistance, especially in the countries that do not have an EU school set-up. Many governments provide financial payments for international school costs for staff of EU institutions. However, many of these schemes have significant delays of when your education expenditure gets reimbursed. Often there can be a gap of 3 to 5 months from payment to getting your money back. If your school costs 1000 EUR per month, that’s a 3000 to 5000 EUR cash flow gap right there. Multiply by the number of kids to increase your headaches. Talk to your school about more favorable payment options to accommodate your budget.

- This is a longer-term solution but might be relevant if you have kids in preschool. You might not be aware that the EU allowance to cover pre-school costs is very small – it’s 91.75 euros per month and gets adjusted by the correction coefficient for your country, so it’ll be even lower than this. Most non-local kindergartens and pre-schools charge between 400 and 1000 euros per month, making it challenging for you to cover these costs from your salary. An increasing number of EU institutions equalize the pre-school allowance with the education allowance (the latter can be either 254.83 or doubled to 509.66 euros). If your institution hasn’t started the process yet, try to initiate a Staff Request to do this. Consult your institution’s Staff Committee about the procedure.

03 | Finance-related solutions

- If you savings that let you finance the extra payments of the first few months, congrats and well done! If your savings are in less-liquid assets, plan ahead to minimize withdrawal fees. However, if you don’t, there are suggestions that might help in your situation.

- Enquire if any relatives could lend you money. Don’t make the mistake of telling them that you’ll pay back in a month, as it might be too short of a period for your cash flow to normalize. Ask for a loan for at least three, preferably six months. If you pay them back earlier, people will be pleasantly surprised.

- While still at your last job, get a credit card with the highest possible credit limit. If you already have a credit card, try to raise it’s limit. If possible, opt for a credit card that has a fixed monthly repayment cap as you are likely to exceed the default payback periods.

- It might be impossible to get a credit card at your new location for some time as you don’t have any credit history and not even a local address at first. However, some EU agencies offer corporate credit cards. These are mostly intended to cover mission (‘business trips’ in EU lingo) costs until you get reimbursed by your institution. Often these can in fact be used for any expense. Enquire at your HR, mission management or corporate services unit.

- If you plan to change cars, don’t buy your new car just before getting an EU job. As an employee of an EU institution you will be entitled to a VAT reimbursement when buying a new car and in some cases even for a used car if bought from a legal entity (car dealership or other business that can issue an invoice) in the country you’ll be working in.

Do you have question or suggestion for this article? Please share in a comment below and let’s make this resource better for you and other readers!

4 responses to “Managing personal finances when starting to work at the EU institutions”

Hi Ben,

Absolutely fantastic site, which has helped me secure a job with the commission, starting in September.

I have a question regarding finances, more specifically tax equalisation. As I am a foreign national moving from outside the EU to a member state, I wanted to know if there is any provision to help in preparing tax returns as I will still be earning money in my home country due to property investments? Is this something the commission helps with due to the unique tax position I will be in once I join?

Thanks

Matt

Sorry for the late reply, I hope it’s till useful.

Congrats on getting the job! And also having a property investment, well done! And – thanks for the nice words!

But, no, COM will not help you with this, as it’s a private matter. There are colleagues in EU institutions that provide assistance to expats to ease settling in in the new location. However, they would not help with this issue.

Also – check with HR if you have to declare this income somehow. Certainly, income from investments is not prohibited, but there might be a need to declare this.

Hi Ben,

Referring to your last paragraph: could you please share a link to the legal basis of the *VAT reimbursement* and/or elaborate how exactly that works and under which conditions? During my internship at an EU institution half a decade ago, I was under the impression that newly established officials are eligible for VAT reimbursement in their first year for larger relocation-related expenses like furniture as well (so not only for cars), but I’ve been looking for the exact rules in vain. For instance, is the 12-months limit I remember correct? What about working people in Luxembourg but considering becoming “transfrontaliers”? Or even if you live in Luxembourg, buying furniture at a French/Belgian/German IKEA will not be eligible for VAT return/exemption?

It looks like I’ll start my probationary period in Luxembourg soon and I would neither want to buy before the end of the 9 months nor miss the deadline because I have no furniture right now.

Hi! I have never worked for the Commission in Brussels or Luxembourg, so I can only share what I’ve gather from friends who work there. Those in Brussels seem to have no limit on VAT reimbursement, but there is a lower limit so it’s for larger purchases. Also, the reimbursed items don’t include food and the like, I think it’s vaguely limited to household items and furniture.

When it comes to the agencies, it depends on how well the agency negotiated with the respective country government. At the absolute minimum, VAT reimbursement is available for the first year to new employees, but there are agencies where the negotiation has yielded better results. There are agencies where the VAT reimbursement is available for a longer period or constantly for certain categories of purchases. Regarding cars, usually at least one car be bought in the first three years of employment. But there are agencies where VAT reimbursement for cars is available every 3 years. In some countries it’s possible to get back VAT only for new cars, but in others also on used cars if they are bought from a legal person (dealership, etc.).

Of course, VAT will be reimbursed only for purchases in shops of the country you work in. However, online shops count as well as long as they are registered in that particular country and issue invoices clearly stating that any taxes were paid in the same country as you are employed in.

Once you start working, VAT reimbursement should be covered in the orientation training or info will by provided by HR. Also ask older colleagues who’ve gone through the procedure.