The opportunity to secure an EU pension is an underappreciated, but a very significant benefit of working for the EU institutions: European Commission, European Parliament, European Council or any of the 40+ EU agencies and several other EU institutions.

The EU pension is a defined benefits/final salary scheme that guarantees you an inflation-adjusted monthly income until your death. Additionally, after you pass away, your surviving spouse will continue to receive a survivor’s pension until her/his death that is a significant part of the pension you were entitled to.

While all of the information below is from public sources, it is often hard to access and understand due to “legalese” and the the sheer size of the documents. This article outlines the main facts about ‘EU pensions’ in an easy to understand manner.

How to qualify for a European Commission pension?

Anyone who works for the European Commission, European Parliament, an EU agency or another EU institution, is entitled to an EU pension after 10 years of service. You have to accumulate your 10 years before you reach either the mandatory pension age (66 years in 2021) or early-retirement age (58 years in 2021).

You can work for different EU institutions at different times in your life. All of your employment periods in EU institutions will be summed up and count towards a 10-year minimum as long as you do not withdraw the accumulated pension capital to a private pension scheme.

The pension contribution (tax) is the largest deduction of one’s salary. 9.7% is automatically deducted from your salary each month to accumulate the pension capital, and no actions need to be taken by you.

What is the mandatory European Commission pension age?

The mandatory pension age is 66, at which you will be able to receive the full amount of pension that you are entitled. It is possible to work until 70 if it is exceptionally justified. After reaching 70 a person is retired automatically and there is no possibility to remain in employment of EU institutions.

How large is a pension after working for EU institutions?

There is a minimum pension for former EU officials. It cannot be less then 40% of the basic salary for an EU official in the AST 1 (step 1) category. In 2023 this amounts to EUR 1331.00 (salary for AST 1 EUR 3327,49 * 10 years of service * 4%).

European Commission Staff Regulations

Hi and thanks for reading the article!

If you found it useful, please consider to

Your pension after the 10 mandatory years of service cannot be less than the minimum pension for EU officials – see above. If you are interested in more detail, the answer depends on a number of factors:

- Length of service. For each year of employment a person is entitled to 1,80% of the final basic salary. For example, if you have worked for EU institutions for 10 years, you will be entitled to 18% of your final basic salary; 20 years will qualify you for 36%; 30 years – 54%; 40 years – 72% (which will be capped at 70%).

- Basic salary in last employment position. Your pension will be calculated as a percentage of the basic salary.

- Pensions are adjusted to the actual cost of living in the European Union and should slightly increase over time.

- The final pension amount may not exceed 70 % of the final basic salary.

If you have worked for several EU institutions, your pension will be calculated based on the last basic salary you received.

In practice, if you are an AD5 in Brussels at the end of your career with a basic salary of 4883, you would be entitled to the following amounts proportionally to the time worked for the EU:

- 10 years = EUR 4883 basic monthly salary X 1.8% X 10 years = EUR 878.94. In this case you would instead receive the European Commission’s minimum pension of EUR 1200.24.

- 20 years = EUR 1757.88

- 30 years = EUR 2636.82

- 40 years = EUR 3515.76

Of course, if you start as an AD 5, your final basic salary would actually be higher as you would advance through the steps of the pay scale every two years. The above calculation is meant to just be an illustration of the principle.

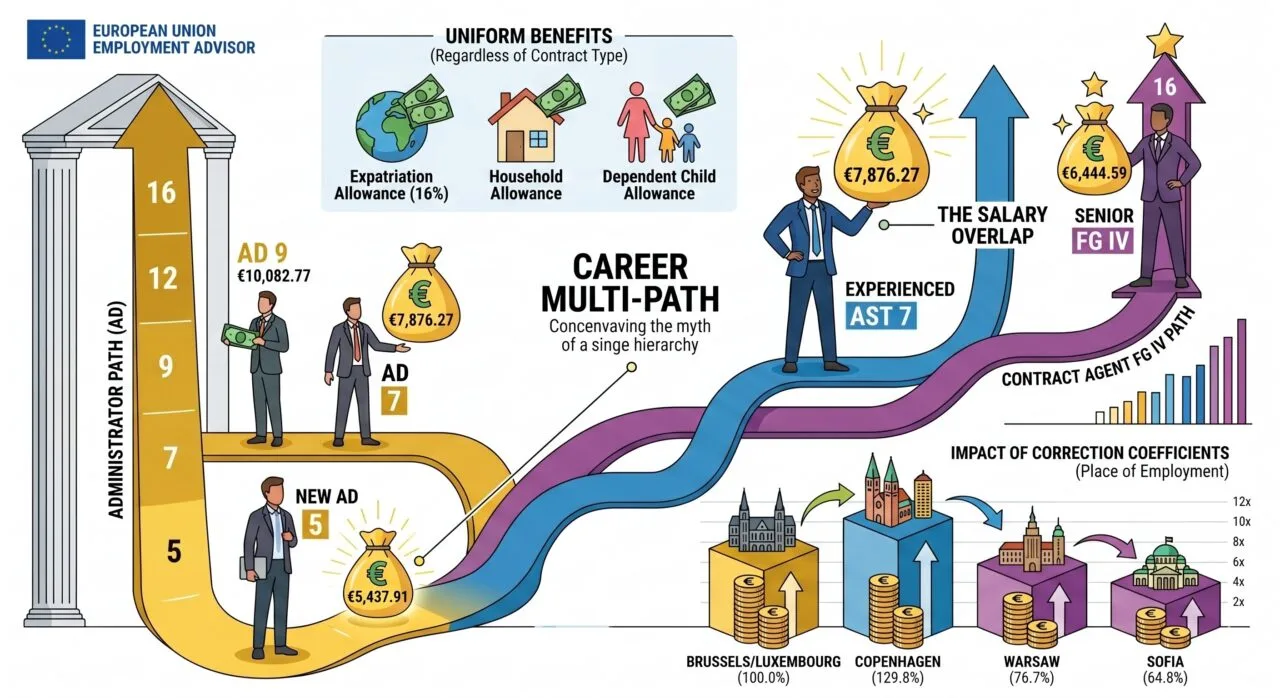

Pensions and the Correction Coefficient

The European Commission Correction Coefficient is not applied to pensions (Article 82 of Staff Regulations). In practice this means that you will receive the same pension independent of where you live after retirement.

Can I retire early? What are the consequences?

The early retiretirement age is 58 years (in 2021).

An early retirement pension amount is reduced 3,5% for every year before mandatory pension age of 66. Hence, if you decide to retire at 58, you will incur a 28% reduction of your pension. Unfortunately, the pension will not increase once you reach the regular retirement age.

Can the EU pension be inherited by a surviving spouse and/or dependent children?

Yes. The surviving spouse of a former EU official is entitled to 60% of the pension paid to the official. The amount that can be inherited by dependent children varies on the individual situation and the ‘orphan’s pension’ can only be precisely calculated by the Paymaster’s Office.

EXAMPLE

If you are entitled to the minimum European Commission pension of EUR 1200.24 (100%)

THEN

your surviving spouse will receive up to EUR 720.14 (up to 60% of former official’s pension) until her/his end of life.

Divorced spouses are also entitled to a survivor’s pension if they can prove that the (former) EU official was supporting them based on a court order or an officially registered settlement in force between both parties.

If you are in such a situation, please contact either the European Commission’s Paymasters Office or the HR Department of the last institution your spouse was working for in order to find out the steps to take.

Very important – unless there are proven force majeure factors, the survivors pension has to be requested within one year of the former EU official’s death. Otherwise, the spouse’s and dependents’ rights are forfeited.

Does my EU pension capital accrue interest while I’m waiting for my pension age?

Yes. The accumulated pension amount accrues compound interest at a rate of 2.9% per year (in 2021).

What if I leave an EU job before I accumulate 10 years of service?

For most people the best strategy is to leave your pension capital with the European Commission Paymaster’s office as it accrues a 2.9% per annum in interest. You can accumulate your 10 years in EU institutions over an unlimited number of instances of working for EU institutions until the mandatory retirement age of 66.

Some institutions strongly encourage the “transfer out” of the accumulated EU pension capital claiming that it might be “very hard” to do it at a later date. However, there is no particular difference in the amount of work for you whether you decide to move your EU pension capital to a third tier pension management fund right after leaving an EU institution or much later. The only caveat – you pension capital left with the EU Paymasters Office will be completely lost if you happen to die before reaching your pension age. And, of course, don’t forget about your pension capital once your retirement age comes and you have not accumulated the necessary 10 years to qualify for an EU pension.

If you decide that you never again want to work for the EU, you can “transfer out” your pension capital to any of the European Commission-approved pension management schemes in all EU member states. The funds will only become available to you once you reach the age of 60.

Reasons to “transfer out” your accumulated EU pension capital:

* You do not plan to ever again work for EU institutions

* You are certain that you will be able to invest your EU pension capital in an investment vehicle that returns substantially more than 2.9% per annum

* You are worried that you might die before retirement age (chronic disease, family health history, dangerous hobby, etc.)

Once you “transfer out” but again start working for a EU institution, you will be able to transfer in your accumulated pension capital, but not the accumulated ‘pension years’ to qualify you for an EU pension. So – choose carefully.

Not only an EU pension, but also health insurance for you and your spouse

After an EU official becomes entitled to an EU pension, the person and his/her spouse and any dependents also become entitled to the JSIS – the European Commission healthcare insurance scheme. It reimburses between 80-85% of most healthcare costs. If you have what are considered serious illnesses you can obtain a 100% reimbursement. This should be a major appeal for people in retirement.

If there are any dependents, the retiree is also entitled to the relevant allowances such as the household allowance and dependent child allowance.

Where to get consultations and help regarding European Commission pensions?

Former employees of EU institutions are usually advised to contact the HR department of the last institution they were employed by.

It is also possible to get in touch with Office for the Administration and Payment of Individual Entitlements also know as the Paymasters Office (PMO), contacts here. If you have questions about JSIS, the European Commission health insurance scheme, including coverage of funeral expenses, you can find the relevant Paymasters Office contacts here.

AIACE – International Association of Former Staff of the European Union

When you retire from an EU institution, consider becoming a member of AIACE. For the 40€ annual fee (differs by location of national units) you can get a number of benefits:

- Access to a helpdesk (consultations on key retiree issues). Virtual and in-person consultations in Brussels

- Legal assistance at a reduced fee

- Special complimentary insurance availability to complement risks not covered by the JSIS (currently offered by Cigna)

- Accident coverage

- Coverage of the difference in all medical costs and those reimbursed by the JSIS

- A monthly Cigna consultation

- Quarterly VOX bulletin sent to all of the retired staff. National bulletins sent to members of country chapters

- Yammer chat

- Voluntary work opportunities and possibility to received help from other volunteers; social contacts and events

Main facts about AIACE:

- AIACE has special Partnership Agreements with the European Commission, the European Parliament, the European Court of Justice, the European Social and Economic Committee, the Committee of the Regions, the Court of Auditors, and the Council. All the above institutions recognize AIACE as the representative of their retired staff

- Founded June 1969, AIACE has over 12000 members out of a total approximately 23500 retired staff

- 15 national branches (20 retirees can form a national branch)

- AIACE lobbies on behalf of retired EU officials and defends their rights at the European Commission and other EU institutions. AIACE is even an official member of a number of working groups that affected the interests of former EU administrative agents and contract agents

AIACE contact details:

- Website: www.aiace-europa.eu/

- Address: N105 00/23, 105 Avenue des Nerviens 00/036, Brussels, 1040, Belgium

- Telelphone: (Belgium): 02.2952960

- Email: aiace-int@ec.europa.eu

Frequently Asked Questions

EU officials have their own pension scheme, managed by the European Commission. This pension scheme serves the former statutory staff of the European Commission, European Parliament, European Council, the 40+ EU agencies and all other EU institutions.

The minimum pension for EU officials cannot be less than 40% of the basic salary for an EU official in the Assistant grade AST 1 step 1 category. In 2023 this amounts to EUR 1331.00 (salary for AST 1 EUR 3327,49 * 10 years of service * 4%).

Yes, pensions of former EU officials are regularly adjusted to inflation the same way as salaries of Administrators, Assistants and Contract Agents. As an example, the minimum EU pension in 2021 was around 1200 euros, but rose to 1311 euros in 2023 as salaries of EU officials also increased.

Mandatory pension age for EU officials is 66. EU officials can retire early from the age of 58, but they take a permanent decrease of their pension for every year of early retirement. Pension of an early retiree does not increase once the person reaches age 66.

Do you still have questions regarding EU pensions?

As usual, if there is an unanswered question or you have spotted a mistake, please write a comments and me and the EUE community will do our best to help and update the article.

This article is based on the European Commission Staff Regulations and other publicly available information such as EU institutions’ vacancy announcements.

183 responses to “Pensions for Staff of European Commission and other EU institutions”

Hi there,

I am a Contractual Agent,I have been working in an EU institution for 10 years. If I change jobs now, am I entitled to a minimum pension when I retire? And if so, is early retirement possible at the age of 58? Will the minimum pension remain after that? Or will the percentage for early retirement still be deducted?

Dear Ben,

I will have an EU pension after almost 30 years of service and plan to retire in a non‑EU country that taxes any income, including foreign pensions, at 40%. Their system subtracts any tax already paid on the pension from that 40%. For example, if the EU taxed the pension at 23%, I would pay the remaining 17% locally.

I understand that the EU taxes its employees’ salaries as one source of EU income.

1.) Do the same rules apply to EU pensions? Are EU pensions taxed at source by the EU before being paid to the pensioner?

2.) If so, what tax rate applies to EU pensions? I assume it would be progressive, where can I find an official calculator or table?

I need these answers before retirement so I can estimate how much of the 40% foreign tax I will actually owe. I know bilateral double taxation agreements (DTAs) are common between individual countries and non‑EU states and would prevent double taxation; as far as I know, the EU as an institution does not conclude DTAs with third countries.

Hello Ben,

Imagine the situation where I am an official and work 10 years in an EU institution and then leave. I am not yet 58 or 66 years old at that point in time and continue to work in a job outside the EU system. Am I later on entitled to the minimum pension and if so, how do I claim it.

Thank you very much in advance.

Best regards,

Sandra

Hi Sandra,

I am not Ben – just trying to be helpful.

If you have worked for at least 10 years in the Institutions, yes, you qualify for an EU pension. You can claim it by writing to the PMO – or they will contact you when you reach 58 or (more likely) 66 years. If I were you, I’d keep payslips and anything which can document your years of service (you never know)

I guess you know that, if you claim the pension when you’re 58 years old, there is a reduction in the monthly amount, compared to claiming it when you’re 66 years old.

Conversely, if you decide to defer claiming it past 66 years old, there is an increase in the amount you’ll receive.

Good luck! And congratulations on achieving 10 years of service in the Institutions!

Hello

If i am to be employed exactly 10 years in total, wirking for various EU bodies, and for the last part of those 10 years, i have a longer period of sick leave (e.g.: 4-5 consecutive months), would this sick leave period be considered part of the.minimum 10 years needed for becoming eligible to get an EU pension and I would be able to benefit of the pension in the end ?

Thank you

Best regards

As far as I know – provided you comply with the rules on sick leave (medical certificates, etc.) – sick leave counts for the minimum period of 10 years.

Thank you for this very informative site.

I was promoted (AST 7) effective January 2025. I had planned to stay the full 12 months so that my pension could be based on new grade. However due to illness resulting in major surgery I took earlier than planned retirement at end July 2025. Just five months short of the required 12 months in grade. Can I ask for a derogation because of illness so that my pension can be adjusted based on 2025 promotion?

Thanks for your feedback.

Hi,

Thank you for a very informative article. I have two further questions please:

Do EU pension payments (paid after retirement) get taxed and by how much?

Do the payments continue until death or until the fund you’ve built up (from the ~9% contributions) runs out?

Hi,

question on Transfers IN:

If I land a job as a TA in a EU institution, and I have previously worked and accumulated pensions rights in an intergovernmental organisation in Europe, can I transfer those contributions to the EU Pension Scheme? If yes, do they count as “years of service and membership” to the EU Pension Scheme and therefore reduce the 10 years?

Thanks

First question – in principle, it should be possible. You could check with the international organisation in question whether they have transferred pension contributions to the EU scheme in the past (and advise you on timing).

Second question – absolutely not. You need to have worked at least 10 years in the EU institutions to qualify for an EU pension. As you may know, EU institutions include the Commission as well as the agencies, the EU Parliament, etc. The 10 years do not need to be consecutive (i.e. you can have a gap between two fixed-term contracts.

thanks Jean-Paul. The answer to the second question is unfortunately very disappointing. Certain intergovernmental organisations allow for transfers IN which also reduce the number of years to mature the right to pension – but I understand this is not the case with the EU.

Hello Laura,

you’re the only one to know your personal circumstances. From what you write, it seems you’re very close to qualify for a EU pension (i.e. to meet the 10-year requirement).

I think it would be good if you could qualify for it – even if it means you have to pay higher rates while on CCP. If I am not mistaken, when you become a EU pensioner, you also have other rights, e.g. reimbursement of healthcare costs across the EU – which is something worth considering.

In brief, if you’re close to the finish line (as you seem to be), it may be worth paying the extra money. Your future self may probably thank you!

Hope this is useful.

Dear Ben,

I was reading a document I found on EC sharepoint regarding EU pension and there seemed to be a mention of a continous contribution to be able to qualify, ie. no break in contracts. However, above you mention that any contribution to the EU pension cummulates until you reach a min of 10 years to be eligible for an EU pension. Could you please clarify what are the latest rules? I had a break of about 50 days between my contracts so I am slightly worried I would need to now start anew! Many thanks, Lenka

Hi there,

I am a Contractual Agent with 13 years of work at EU institution and I am very confused on this early retirement as a Contractual Agent – so, not as official.

On one part, you and PMO.2 pension state that one can leave work at EU Institution before they reach early retirement age, and that they can claim their pension once they become 58 years old.

On the other part, HR pension team of my Institution state that, for example I will not be able to claim my pension at the age of 58 ( I am now 56) if at the time I am not actively working. Please read the HR pension team reply here below:

REPLY from the HR PENSION TEAM in my current Institution:

”Article 9 of Annex VIII says:

An official leaving the service before reaching retirement age may request that his retirement pension be:

– deferred until the 1st day of the calendar month following that in which he reaches retirement age

– Immediately, if he has reached the age of 58. In this case, the retirement pension is reduced according to the age of the person concerned at the time when his pension starts.

So, if you are not working in a European Institution when you reach the age of 58, you will not be able to take your pension at the age of 58.

You will have a deferred pension at your normal pension age.

The situation will be the same if you benefit from unemployment allowances of the European institutions. ”

I am puzzled and worried: What happens if I will not find another EU contract until I am 58 years of age? Will I be not entitled to claim my pension when I get 58?

Thank you very much for your reply and support and all the best,

NIcoletta

Hi! I have worked about 8 years in the institutions so would be able to qualify for the EU-pension in a bit more than 2 years. However I possibly may need to leave the institutions before that, I know it would be best to stay until I secure it but life is not always easy. What would be your advice in my situation if I leave before obtaining my 10 years as I only need a bit about 2 years to get it? I may return to the institutions someday but I am not sure where life will take me. As I am quite close to the 10 I am guessing it would be wiser to choose for opt-in in case I do come back? Or is there another option that may be viable? Thank you!

Hi Laura,

are you an official? in which case you may be able to ask for CCP – unpaid leave – for up to 12 years. This will give you time to see how your situation evolves.

Even if you are not an official, there may be types of unpaid leave you can ask for, which will give you some flexibility.

If you do leave, I would advise to leave your “pension pot” with the Commission. As you say, you may return to the Commission in the future and then you’ll only need two years to qualify for a pension. Those eight years will still be there waiting for you.

Best of luck!

Dear Zac,

Thank you for your helpful reply, I am a temporary agent and have been looking into the unpaid leave option, as TA you can take 1 year max. Your accumulation of pension stops during that time but there is an option to let it run if you cover the contribution yourself, however the % is considerably higher when you do this (9,7 becomes 36% if I am correct). Even though the cost is very high I think it may be a good course of action if you only have 1 year or less left to bridge and highly doubt you will return to the institutions. Any thoughts on this?

Kindly clarify, if possible how the basic pension is calculated if the minimum of 10 years of service are completed at age 53, and then I resume a national employment until 66 years old.

Is the pension at 66 based on the acutal salary numbers of that future salary level or my last salary of the employment at age 53?

Also for the transfer in procedure is there a maximum number of equivalent years that can be achieved with my national funds etc?

i.e. if my national pension funds are big enough could they be counted as e.g. 30 years?

Many thanks for your clarifications!

Thank you for an invaluable resource.

I have a question on the transfer-in process. I have a UK-based private pension fund with one of the largest fund managers there. I would like to transfer that in the EU system where I now work. I understand this right is not guaranteed, and also that it can take a very long time (several years, apparently) to have a reply from PMO after making a request. Is this true? It would be difficult to make retirement/career plans during that time. Also, the value of the fund fluctuates over time, up and down. How would fluctuations be treated between the time I make the request and the transfer, if accepted?

Brian, hi! I assume you have a double nationality… or you’re using the post-Brexit arrangement where UK nationals with contracts prior to Brexit were allowed to stay and work in EU institutions.

Anyways –

1. According to my understanding you would have to first get 10 years of service in EU institutions. Only then you can transfer in your pension capital and increase your EU pension. I understand it’s not possible to serve the institutions for, say, 7 years and get the remaining 3 by a ‘transfer in’. If you have your 10 years, read on. The only exception would be if you’d reach 66 as the legal retirement age during EU institutions employment before 10 years of employment overall.

2. Regarding a transfer in, the institutions still struggle with post-Brexit legal arrangements, due both to EU-side but also UK-side issues like lacking legislations, rules of procedure and case law. Due to this I suggest that you write a formal question to PMO. This would give you the highest level of legal certainty. PMO contacts: https://commission.europa.eu/about/departments-and-executive-agencies/office-administration-and-payment-individual-entitlements_en#contact

All of the above is correct.

Specifically regarding the original question: My understanding is that it IS possible to transfer the capital value of the UK state pension into the Commission’s pension scheme. This is a transfer-in, which needs to be requested before 10 years of service. In this case, the UK DWP says “this person’s pension is worth 10k GBP” and then PMO says “OK, that is the equivalent of 2.5 years of Commission’s pension, which can be added to your years of service”. At this point, it is the original poster’s choice to go ahead with the transfer-in or not. All figures above purely illustrative.

HOWEVER, if the original poster is talking about transferring a SIPP (self-invested personal pension, which can be invested in stocks, funds and bonds and therefore its value fluctuates every day) into the Commission’s pension scheme, that is virtually unheard of. I am not even sure that a) the SIPP provider in the UK is able to execute the transfer and b) the PMO is able to accept the transfer.

At the very least, the original poster would have to sell all its holdings and willing to hold cash from the time the request is made until the transfer actually happens. As I said, I am not even sure the transfer is possible.

This is my current understanding, but any additional information (from PMO, perhaps?) is welcome.

As a final note, this scenario is not limited to UK nationals. Any EU national working in the UK can open a SIPP and then, at some point, be hired by the EU institutions. At this point, the question arises of what to do with a) the SIPP and b) the contributions paid in the UK to qualify for the UK State pension.

Thank you for the reply. I will consider asking a question to PMO, because this has a large impact on the benefit of my staying with EU institutions for 10y (and acquiring the right to a EU pension) or not.

In response to John Smith below, I am talking of a UK ‘workplace pension’, not the UK State Pension and not a SIPP. This is a very common scheme – the norm for employees in the UK private sector (on top of the UK state pension, of course). It is invested in funds which fluctuate. I have heard of individuals having this transferred in, but it was pre-Brexit and I don’t know the details. And it’s correct that the nationality of the employee is irrelevant, since anyone who has worked in the UK private sector is likely to have a similar pension.

Hopefully, the PMO will be able to clarify the issue.

As I said, it is possible to transfer your contributions to the UK State Pension into the EU Pension scheme.

When it comes to personal pensions (whether they are workplace pensions or SIPPs), things are much less clear. If you can share it, useful to know who your provider is (e.g. Aviva, Fidelity, etc.). And whether they have confirmed to you that they can execute the transfer (possibly after you sell all your assets to freeze their value in monetary terms, i.e as cash).

Good luck! It’s such an important piece of the overall puzzle – and yet so little information is available.

The way I understand it, a UK pension scheme can pay into a foreign scheme with no UK tax charged as long as the scheme is a ROPS. The EU Civil Service pension scheme seems to be one, but I would need to confirm that. Technically there should be no impediment to the UK side paying out, since workplace pensions can be entirely cashed in. It’s UK tax that may be the question (hopefully avoided if ROPS) and especially whether PMO accepts the transfer. I don’t see why it shouldn’t – a transparent fund value is easier to convert into years of EU service than years in a member state. But you never know.

The Commission’s pension scheme is indeed a ROPS – see here: https://www.gov.uk/guidance/check-the-recognised-overseas-pension-schemes-notification-list#countries-d-to-f

Whether any transfer out would be tax-free is not clear at all (the site mentions that rules changed in 2017… anything happened in that year or the year before? 🙂

And then there are the questions of whether the pension scheme administrator is able/willing to execute the transfer and whether the PMO will accept the transfer. And of course the time needed for all of this to happen.

Dear Ben, i have been on an invalidity allowance for 3 years due to serious illness. Are these years eligible for the 10 years of service. I had the option to keep on contributing to the pension scheme, which i chose to do.

Thank you.

Hi, Andre! My understanding is that the pension is NOT adjusted by the correction coefficient, i.e., you should get the same pension irrespective of where you live as a retired principle. In this sense the arrangement is similar to the EU unemployment allowance which is also not adjusted by the CC.

My understanding is that the EU pensions are adjusted by the correction coefficient. I do however live in a 100% coefficient country (Belgium) so I cannot confirm this via personal experience

Hello, gongrats for your insights. I would like to ask if it is possible for a person with less than 10 years of service in an EU institution to opt for leaving contributions accruing in the EU pension system, getting them later at the age of 66. Is this option available or in these cases (less than 10 years), it is mandatory to transfer out your contributions to the national scheme?

Thanks in advance!

Hi, Mike! My understanding is that it is possible. You can withdraw your contributions residing in the EU system at any time, but you can only gain access to the capital at the age of 58 if you opt for an early retirement. There are many cases where former EU institutions’ staff say they were “forced to” transfer out their capital at the time of leaving their institution. However, this seems to be more of manipulation and people gave in.

Hello,

I have already worked enough years to secure a pension, but I am contemplating taking a break for a couple of years to pursue another paid activity. For that I would ask for a leave on personal grounds (CCP).

I would like to ask if I may “buy in” the pension rights I acquired during that leave when I resume my job at the EU institution.

Thanks for your help,

Maria

Hello Maria,

this is a tricky question – Have a look at paragraph 3 of article 11 of Annex VIII (Pension scheme) of the Staff regulations:

https://eur-lex.europa.eu/legal-content/EN/TXT/HTML/?uri=CELEX:01962R0031-20140501#tocId248

“Paragraph 2 shall also apply to an official who is reinstated after a period of secondment under the second indent of Article 37 (1) (b) of the Staff Regulations and to an official who is reinstated following expiry of a period of leave on personal grounds under Article 40 of the Staff Regulations.”

I say it’s a tricky question because paragraph 2 includes the “before becoming eligible for payment of a retirement pension”… and you have already become eligible because you worked more than 10 years in the EU institutions.

What I am thinking is whether there are two scenarios: one where you go on CCP, say, after working for 5 years; and another one (which is your case) where you go on CCP after 10 years. With two different outcomes.

Not sure whether this helps – better check with PMO for a definitive answer.

Hi! The best thing is to attend one of the PMO seminars about pensions. If your HR doesn’t share this info about seminars, ask them proactively. PMO always encourages to write to them directly. PMO contacts: link to COM website

Dear Ben,

I am currently exploring the option of transferring my national pension contributions into the EU pension scheme and would appreciate clarification on the following matters:

– In my national pension scheme, it is possible to make additional contributions to account for years spent in education or military service, thereby recognizing those periods for pension purposes. If I transfer my national pension contributions into the EU scheme, will such years also be recognized under the EU pension system?

– Is there a requirement to have completed the minimum 10 years of service within EU institutions before initiating the transfer of pension contributions from a national scheme, or can the transfer be applied to help secure the 10-year minimum required for EU pension entitlement?

– In order to calculate if the transfer will be to my benefit, would it be possible please to let me know for each month after reaching the 10-year minimum threshold for an EU pension, how much does this increase the final pension benefit?

– Upon transferring national pension contributions into the EU scheme, are the corresponding years of pensionable service recognized in full as they are, or is their value adjusted in line with the EU pension contribution system?

Thank you for your assistance.

Petros, hi!

As far as I know, you don’t transfer “years” into the EU scheme, but pension capital which is “equalized” to your contributions while working for EU institutions. Because of this it’s very likely that 10 years in an EU member state pension scheme might turn out as 5 years or even less in the EU scheme. Best to ask PMO and national pension authority to do a calculation to decide if transfer in is beneficial for you.

You have to collect 10 years of working for EU institutions before you can transfer in.

Each year of working for the EU gives you a 1,80% increase in the final pension. Quoting the article:

“Length of service. For each year of employment a person is entitled to 1,80% of the final basic salary. For example, if you have worked for EU institutions for 10 years, you will be entitled to 18% of your final basic salary; 20 years will qualify you for 36%; 30 years – 54%; 40 years – 72% (which will be capped at 70%).”

You qualify for the minimum EU pension without reaching 10 years if you reach pension age of 66 years while working for an EU institution.

Hi, great article answering questions. From my experience, I had worked in organization for 2,5 years, had to do a break and was “forced” to take the pension contributions that I collected over those 2,5 years. Why I say “forced” – no other option was proposed, I just received an email saying that this amount will be sent back to my account… so I took it… Now I am back at the same organization and thinking of doing the minimum 10 years to get the pension, but those 2,5 years will not count. Asking around at work everyone is saying that it has to be 10 consecutive years, I guess this rule that it can be done in multiple instances is just not shared widely.

PMO really can’t force you to “transfer out”. Too bad very many people are manipulated this way.

I now it’s possible to transfer in your national pension scheme contributions. I wonder if it’s possible to transfer back in the previous EU pension scheme contributions that you’ve transferred out. Definitely something to look into.

You most definitely can collect the 10+ years in several “instalments”. I’ve checked with PMO.

Hi Ben and Simon above,

I cannot be certain but I am pretty sure I read that it is alwaxs psossible to do a transfer in after a transfer out, at least in the case of a transfer out to a private fund.

In other words, as far as I know if you transfer out to a fund then get beack to any EU institution you should be able to recover the constributions and pay them in the EU pension scheme.

Please don’t take my words as gold, better check it out with PMO…

Hi Ben and everyone,

For once I can help rather than ask for it..

Time ago I mentioned here that when you intend to transfer out your retirement contributions (if you have worked less than 10 years, of course..) there may be some countries which require to do so within 6 months from end of contract.

Well, after a lot of enquiries I have the following information:

– In the case of Spain, Belgium and Italy there is no 6 months rule; HOWEVER, what I have been told by all three is that if you want to transfer out to any of these three national schemes you can ONLY do it if you get a job in the country of interest AND within 6 months from 1st day of work there!

In other words, if you plan to retire early, or just can’t find another job, the only possibility is to transfer to a PRIVATE fund, such as Monet/Allianz in Belgium for example.

I hope this helps!

Dear Alessandro, thanks so much for sharing back!

This is an important nuance that should be updated in the article – transferring out to a private fund (also known as ‘3rd tier pension fund’) and the national pension scheme. I was not aware of the restrictions imposed by the national institutions, as the PMO webinars seem not to cover this aspect. So – it’s up to each person to inquire with the national state pensions authority.

Hello,

I have been working for the Commission as a DNE for nearly 4 years (2011-2014) and then for 6 year as Contract Agent. Does this DNE work count in this required 10 years in order to have the right for an EU pension? Thank you

Sorry, no, SNE employment period doesn’t count towards the EU pension. However, hey, at least it counts for the national pension. And then, if you’ll work for at least 10 years total for EU institutions, you can transfer in your national pension.

Dear Ben,

I worked for an EU institution one year only, then I resigned after the contract renewal to go back home and work there. I haven’t transferred out anything yet, and I am 54.

Do you think I can still claim my contribution regardless of my interrupting the contract?

Thanks in advance for for your help!

Kind regards regards,

Claire

Of course. You are entitled to the pension contributions and can either transfer them out or leave them in the EU system. The only instance when you can loose this amount if you suddenly die. If you do not plan to work for EU institutions ever again, I’d transfer out to a private pension fund so that in case of your unexpected death your relatives could inherit the amound. If you haven’t transfered out and suddenly die, the money is “lost”.

Hi all,

I worked for an Institution for 1 year and 3 months. I then stopped for a while, before moving on to another Institution, where I currently work.

I’ve been here for 2 years, and may stay here for another 4, for a total of 6. There haven’t been EPSO competitions for years, and one cannot rely on there being one in the near future.

Therefore, the gameplan is to face the possibility of retiring in 2029, with 7 years of service in total. At that point, if the 10 year = pension strategy is not possible, I would dearly like to access the funds that I contribute towards every month from my own salary.

Would the small gap between jobs prevent me from doing so? I would be able to use them to secure my financial position in retirement far better than leaving them with the PMO until 65 ever could. I pay pension contributions in my country.

Thank you,

Godfrey

Hi! If you haven’t reached 10 years of employment in total for EU institutions, you can always transfer out the 7-year long pension contributions to either your national primary pension scheme, or a private pension fund.

Importantly – I can’t find the precise stipulation in the Staff Regulations, but I believe that if you’ve worked for EU institutions less than 10 years but reach retirement age while being employed at an EU institution, you’re entitled to the minimum EU pension which is 40% of basic salary in grade AST 1 step 1 (AST1/1 amount for 2024 is EUR 3461,58 (Source is Article 66 of the 2024 Staff Regulations edition), hence 40% of this would be EUR 1384.60.

Hi! This is not correct, according to the answer I got from the EP Pensions and Social Insurance Unit: ‘You will be entitled to the minimum: AST1.1 x 4 % x number of years of service.’ In my case I will have been working 3 years in total, when I reach my retirement age.

Anders, thanks so much for sharing!

Would it be possible for you to share an anonymized response from HR to info@euemployment.eu. I’m wondering if there are more details in the reply and references to legal documents.

Hello, I receive 100% of an orphan’s pension. But I would like to start a company. I live in Germany and would therefore like to set up a limited liability company (UG). As this is a legal entity in Germany, I would like to know whether orphan’s pension recipients are allowed to set up a UG. As the sole shareholder, I would then only be paid out as much as I am allowed to receive each month (1200€) before tax (based on my current pension) and leave the rest in the UG. Am I allowed to do that? As far as I know, assets are irrelevant when it comes to paying out the pension. And the UG would be an asset in this case.

Because it is such a special case, it is incredibly difficult to find information about it.

Tax or business consultants here in Germany do not know anything about orphan pensions. And the pension office does not know anything about German law. I am so desperate. I have also asked the EU several times, but I never get a proper answer or sometimes I am told yes, sometimes no.

I am so desperate that I would even pay money if someone could help me.

Dear Herber,

This is indeed a very specific case. However, here’s a tip that can help.

You should address HR of the EU institution in which your parent was employed in writing. Explain the case and asking to provide a legally binding explanation. You can also address PMO, the Paymasters Office of the European Commission. Or write to both and ask them to reconcile which is the proper institution to reply to your question.

You should to the same with the German pension authority. I would first wait for the reply from HR/PMO, and then forward it to the national institution together with your question. In most EU countries there is a special administrative law provision that allows you to ask for a legally binding reply. If you have then acted in accordance with the state institution’s response, but the institution’s interpretation turns out to be faulty, you can claim reparations from the institution. I’m certain German law has this, so please ask a person who’s better versed in German administrative law.

Dear Ben,

I am Dutch and have been working in The Hague under the EU Commission for 6 years and have built up an EU Comm Pension over these years.

I am in the process to have my EU Comm. Pension transferred out but

I was informed by my Pension provider that once finalized the monthly payments that I will receive could be taxed with 19, 37 or even 49% depending on my personal situation.

Now here is my question on which I have not been able to get an answer until now:

I seem to remember, but I am not 100% sure of this, that the contributions that I made to the EU Comm. Pension fund on a monthly basis were already taxed and there for would be exempt from additional taxes ones used for a monthly pension.

Do you know if this is correct or not?

Thanks in advance and kind regards,

Max Schmits

Hi! Indeed, according to EU law, the pensions should not be taxed just like your EU income. However, there are a number of EU Member States that tax not only pensions, but also try to tax salaries of staff of EU institutions.

I can suggest several courses of action if you really decide to transfer out (i.e., you’re certain that you won’t collect additional 4 years in institutions to get the EU pension):

* transfer the funds to a 3rd tier pension fund in a different EU member state where you are certain that the payouts are not taxed.

* try to find a group of your nationals that have the same problem and consider litigate together. Here AIACE, the former EU civil servants’ union, could be of help with contacts and possibly also advice.

If possible, please let me know what action you decide to take and how it plays out! Also – consider joining our new Facebook group (https://www.facebook.com/groups/jobs.in.eu.institutions). While it’s small, it has a health growth and there might be people in a similar situation who can share their info and expertise.

Hi!

Apologies if I am misunderstanding your situation.

I thought that, when you transfer out your EU contributions (say, 40k euros) into a national scheme, then the pension you receive from the national scheme in question is taxed according to national tax rules and rates (so, perhaps even as high as 49%, depending on your other sources of income, e.g. if you’re still working after pension age).

In other words, since you’re receiving the pension from the national scheme and not from the EU, the exemption from national tax rules which applies to EU pensions (after 10 years) is not applicable in your case. It is a national (Dutch) pension – not an EU pension.

That’s my understanding – but I may be wrong.

Dear Ben,

I already bothered you on the forum on unemploymen benefits, and since your answer was extremely clear here I am again, and always thanks for the patience!

My question in three parts:

1- just to be extra sure: having worked only 6 years for the EC they cannot force me to transfer out my pension rights, correct? At least, for as long as I am not old enough to retire..

2- I think I read in one of the answers that when you reach a certzain age (55 or 58, not sure..) you can ask the PMO for the whole lump sum corresponding to your pension rights from the EC, is this true?

3- I heard a lot of rumours about a time limit for the transfer out depending on the country: for example, according to the trade unionist at my last Ec working place, in the case of Portugal you only have six months after end of contract! Do you know anything about this type of country-dependant time limit, particularly in the case of Belgium?

Thank you so much, there should be a statue of you in Berlaymont…

1. I’ve heard many stories about colleagues being “forced” to ‘transfer out’. However, I’m not aware of any legal basis that would allow forcing people to leave the EU pension system. I personally would just ignore such requests if I had a plan to collect the minimum 10 years of employment in EU institutions or wasn’t sure that a 3rd tier private pension fund would to a better job than PMO.

2. One can access the pension capital at the age of 55 if you have ‘transferred out’ your pension capital to a private third tier pension fund. If your pension capital is still with the PMO, then it’s my understanding that you can only request an early retirement from age 58 and a correspondingly decreased pension for each year of early retirement before age 66.

3. I’ve attended several PMO pension seminars. It’s always shared there that transferring out can be done at any time until reaching the pension age.If something has changed, it’s a very recent change in this case.

Dear Ben,

referring to the staff regulation

“He shall, however, be entitled to such pension irrespective of length of service, if he is over pensionable age,”

I have 3 questions please:

Is pensionable considered to be the 58th or 66th year of age?

Is the minimum pension then increased in case that you transfer-in (I have 10 years from Germany which I could transfer in).

And without any transfer-in, which is the amount of minimum pension, given that you have not completed the 10 years of service in the Institutions?

Thank you

Hi Ben,

is there a disability/invalidity pension scheme for those who have to drop out due to permanent illness?

Hi Ben,

Please help me to find out where could I get exact information about how much I accumulated in my “pension account”. I worked for 3,5 years at the European Parliament’s Secretariat in Luxembourg as Contract agent and Temporary agent on various positions. As I get it correctly, I can withdraw the whole amount, or transfer it to my national pension scheme when I reach retirement age. Thanks, Gabriel

Gabriel, hi! You should write to either your last institution’s HR department, or straight to the PMO Luxembourg office. The following contact details should work: PMO-RCAM-LUX-RDV@ec.europa.eu or + 352 4301 36100 +32 2 29 11111. The phone working hours are usually very short so try in the morning from 9:30 to 12:00. Hope this helps!

Hi Ben, thanks for your really helpful website.

I have a question regarding the survivor’s pension and hope you can help.

Does a survivor receive 60% of their spouse’s EU pension when they themselves already receive a state pension?

As far as I’m aware, the answer should be a “yes”. If you have earned the pension rights, there’s no reason for them to go away because of a parallel entitlement.

However, it’s safest to enquire with the PMO or your institution’s HR.

From your article: The accumulated pension amount accrues compound interest at a rate of 2.9% per year (in 2021).

Can somebody explain to me how this compund interest will affect my pension when I worked for the institutions 10 years and I will get only the fixed minimum pension?

Hi Ben, will a child of unmarried parents get orphans pension from. Say an eu retiree who has a child but was not married to thw childs mother. Will such child be entitled to orphans pension?

Hi! Entitlement to child-related allowances and benefits is not linked to parent’s civil status, but paternity/maternity. Hence the answer is yes.

Deal Ben,

I worked in a management position for several years but then moved to a non-management (adviser) position a few years before retirement. Do I lose the management allowance completely for the calculation of my pension of is is taken into account on a pro rata basis?

Thank you

Stefan

Hi! This would be a question to your institution’s HR or the PMO. I believe PMO only takes the basic salary into account when calculating the pension amount, but I might be wrong.

If you enquire with HR/PMO, please let us know what was the response.

I think I should establish a Facebook group, where it would be easier to have discussions on questions like this.

Hi Ben,

I would like to know if you can still perform paid work after retiring. Could the amount paid be deducted from your pension?

Best regards,

Maria

There are plenty of officials who have retired (and receive a pension from the EU) and continue working. One example for all – the former Secretary General of the Commission:

https://www.arnoldporter.com/en/people/i/italianer-alexander

(you are still required to comply with the staff regulations, e.g. on conflict of interest)

Thank you so much Max!

Thanks for this article. Is it incompatible to receive the EU pension and another pension as well?

If you have qualified, you can receive a pension from another source in parallel to the EU pension. While it is not encouraged by the EU, some staff continue to pay national pension contributions during their period of EU employment to also get national pension entitlement. This probably makes most sense if you have 10 or less years remaining to qualify for a national pension. Also – there is nothing to prohibit you from taking part in the so-called 3rd pension tier funds, where you make a fixed payment every month and then it gets invested on your behalf.

I would be much obliged if you could advise whether former contract employees of European Union Missions in Kosovo, Bosnia or Somalia are entitled to pensions where they were in continuous employment for years in some cases over 8 years.

Apologies, but I know very little about EU missions. Could you please contact the mission’s HR or the Paymasters Office, PMO?

Dear Ben,

you write in your article: The accumulated pension amount accrues compound interest at a rate of 2.9% per year (in 2021).

How does this actually affect my EU pension? Because you write in other parts of article that: your pension will be calculated based on the last basic salary you received.

Is there any extra amount added to my monthly pension then?

Thank you

Once you start to receive your pension, it is indexed at least once a year, usually, in December. You might then get a retroactive extra payment due to inflation (and there is the theoretical possibility of a deduction from a pension due to deflation).

Hello Ben

Thanks for the article, amazing!

I get that once pension is taken early, say at 58, it stays at the level and there is no ‘jump’ at the normal retirement age of 66.

Would you know though if the pension, once in receipt, is adjusted in line with an inflation index? Or alternatively, if the 2.9% compounding mechanism applies to the pension also when a person is already retired? I would imagine that there is an inflation protecting mechanism but thought I would confirm.

Thanks again for the great content!

Maciej

Hello Maciej,

I don’t work for the European commission, never have, probably never will. However as dealing with my parents divorce and associated alimony, my father (who worked for the European commission) I’ve had to contact the PMO to sort out pension, alimony and indexation.

I’ve had it confirmed to me in writing that:

“We do not pay an indexation according to the national increases. The indexation for both active and retired staff takes place every December with a retroactive payment to July of the same year.”

It has also been confirmed to me that been confirmed to me that this refers to “the indexation of people receiving a retirement, survival or invalidity pension from the EU institutions.”

Hope that answers the indexation question for you. For the 2.9% i can’t assist however.

Kind regards,

Martin

As Martin replied, pensions are indexed. However, this is a specific EU institutions process that usually lags behind actual national inflation/deflation statistics.

Hi Ben,

Thank you for your very informative article. Do you know whether the years someone works part-time (80% or 90%) while still paying 100%/full-time pension contributions count as full years of service, i.e. towards the 10 year minimum after which a pension can be claimed?

Many thanks,

Michael

I’ve just got an answer to this from the Pensions Department in the EU institution I work in. The answer is ‘yes’. I thought it would be but preferred to ask a possibly silly question than to discover later that I’d have to work a few extra years!

Thanks again for you excellent site and for the advice you provide.

Thanks so much for taking the time to share the PMO reply!

Dear Ben,

Your article is greatly helpful and informative. I thank you for your personal effort and time invested. I have a few questions about my future pension rights with the EC, questions that may be interesting to other readers as well.

1)I am currently 46, married, with 1 child of 2 years, so I currently receive the household allowance and the dependent child allowance. In 3 years, I will have 10 years of service as EC official (contract agent).

Does this mean, if I stop working with the EC after having the 10 years pension right, that I can request to receive at the age of 58 the pension monthly amount of 1200.24 minus 28% = 864 euros, plus household allowance (if still married at that age) plus dependent child allowance (provided that the child’s age permits so)?

2) If I leave the EC after a total of 10 years of service, and I don’t transfer out my EC pension right, will this affect my national pension scheme? ie. If, at the age of pension in Greece, I don’t have enough pension years (if the EC years are not to be taken into account, since I won’t transfer them out (to Greek pension scheme), does this mean that I might not be eligible for a national pension?

I hope I have been clear. I am a bit confused on how the EC pension and the national pension work together.

Thank you very much in advance. Take care.

Hi!

1) Yes. That is also how I understand the rules. That’s the pension amount, you will keep on getting the child allowance. You will also entitled to the education allowance if applicable (covers also university studies at double rate). Once you retire, your spouse and dependents also get JSIS coverage. Bear in mind that the pension amount will not increase as you age, it will stay at the early retirement amount (which really sucks).

2) If do not transfer out, of course, you will not get additional rights in the national pension system. The best thing to do, once pension nears, ask for a precise calculation from PMO and the national system. You can also transfer in national pension rights, but they are not counted in years, but in financial capital.

If this is relevant, ask your HR when is the nearest PMO pension rights webinar. Those are really good and you can follow-up with questions to PMO colleauges after the webinar.

Thank very much you Ben! Be well.

Hi Ben thanks for the info.

One more explanation needed: if we worked in an EU member state before joining the EU Institutions but we did not reach the minimum period requested in some MS (like in Germany is 5 years), but we did not want to transfer IN the EU scheme this previous contribution, it was said by PMO that the pension authority of that MS has to take into account years worked in the EU institutions to reach the minimum period and pay a pension pro-rata. Do you have any further information/evidence about this? thanks in advance

Sorry, this is too specific, you would have to ask PMO or the national institution.

Hello Ben,

you are very clear.

I have only one doubt and I hope you can clear it up for me: in a few days I will go to work in Brussels (moving from Spain). When I will be eligible for the right to a pension, would my expatriation allowance and family allowance be paid to me together with the minimum pension of 1200 euros, although my residence remains in Belgium?

Thank you!

Household allowance seizes to be paid. You will continue to receive dependend child allowance if you children are in your care. If they atttend a for-a-fee school or university, you will continue to receive the education allowance until they graduate or reach the statutory age when the allowance stops.

Hi! Thanks for your articles – very useful!

A question regarding the 10 years necessary to qualify for a EU pension – does CCP count to that effect?

Say, a person who has worked for 6 years in an EU institution and then went on CCP for 4 years – is she entitled to the pension (albeit to an amount corresponding to her last salary in the EU institution)?

Thanks!

Could you please clarify what does CCP mean? I think it was one of the EU’s special missions to third countries, but am not completely sure about this.

If that’s what you mean, another reader recently pointed out that it really depends on the contract. Staff of CCP missions usually are not statutory staff of EU institutions, and hense this work experience doesn not count towards 10 minimum years to qualify for an EU pension. However, looking forward to your clarification and also info about what type of contract you had.

Sorry, CCP is the french acronym for “Leave on personal grounds” – art. 40 of the Staff regulations. I was an administrator (AD).

Hello Ben and Francisco,

I’m taking the liberty to jump in here as I looked into taking a “Leave on personal grounds” recently to follow my spouse and was interested in maintaining my pension contribution at that time. I had read that TAs could pay upfront their pension contributions themselves for the duration of the CCP. However, that only applies to certain type of TA contracts TA of 2C type and 2d (I discovered on this occasion that there were different TA contract types). For my type of contract TA 2f, this is not an option unfortunately. Here is the written reply I received from DG HR:

‘It is possible for a TA2f on unpaid leave to continue to contribute to the sickness and accident insurance schemes only if they are not working or are working but cannot be covered under any other scheme.

It is not possible for a TA2f to acquire pension rights during a period of unpaid leave.’

Hi,

I just have a basic question. As an EU Commission official I have my pension rights secured after 10 years and calulated as explained above.

Now, according to the treaties the salaries of EU officials are not subject to national taxes. What about the pension? Is taxed according to the rules of the country of residence of the retired official?

Thank you

Dear Filo,

Same community tax principle applies for the pensions so not according to the country of residence.

However the country where you will take your retirement residence has an influence on your pension coëfficient and thus can in- or decrease with the same level of rights accordingly the final amount.

As far as I’m aware, the correction coefficient is not applied to pensions. You get the 100% Brussels amount irrespective of where you choose to retire. This can also be a third country.

Pensions are also not taxed in the home country. EU countries are generally aware of this. If you run into issues, you must contact PMO and ask for assistance. Issues appear to pop up from time to time, but these most often individual cases related to banks, overzealous state institutions staff etc.

Dear Ben, my wife has been working for the Commission for the last 17 years as a temporary agent. We are getting a divorce and as a spouse I need information about my pension rights and also my JSIS coverage. I don’t have access to the system and I don’t know who to contact. I am sure there are many spouses that have the same problem. I would really appreciate your help.

Dear Tobias,

Unfortunate to read what you are going through. Although it is a general answer I am giving here; I am afraid that you are not entitled for any pension right as its entitlements are linked to the person who worked for the Institution. The JSIS coverage (full/complementary) will cease to exist in the end too.

In such case you will have to check / enroll with the (un)employment/social wealthfare office of the country you reside in.

If you believe you have a particular case or for a more accurate info, try the contact details you find here in the link below:

PMO – Rights, salaries and allowances:

https://ec.europa.eu/pmo/guide/rights-and-allowances.html

JSIS – Welcome Desk/Hotline:

https://ec.europa.eu/pmo/guide/jsis-request-of-information.html

Erik, thanks so much for helping to answer to questions! ❤️

Tobias, hi! If you divorce, you are most likely using the rigths to the survivor’s pension and also JSIS coverage when you retired as the spouse of a retired EU official.

If you want to have official information, you must write a letter to PMO, the Paymaster’s Office of the European Commission. You will find contacts of the relevant unit here: https://ec.europa.eu/pmo/

Dear Ben,

Thank you so much for the effort in collecting all this info in one article! It is much appreciated.

I would like to ask you a question that arises from the wording you are using in the text. More specifically, you mention: “The mandatory pension age is 66, at which you qualify for a full EU pension”. When you write “full pension”, do you mean 70% of your last basic salary, or the pension corresponding to (number of years worked) X 1.8%?

I hope you will find the time to respond but, regardless, thanks a lot for all the info provided 🙂

Cheers,

Nikos

Nikos, thanks for the question. I meant “the pension corresponding to (number of years worked) X 1.8%”. Will try to specify this more clearly in the text.

Sorry about delay in replying, lots of work lately.

Hi Ben

I am a temporary agent with 8 years contemplating resigning and leaving the institutions for good. I’ve roughly worked out a transfer value of approx €200k capital value. I’m in my early 40s.

It’s unlikely that I’ll ever work in in an EU institution again to make up the ten years so I’m considering a “transfer out” to a private pension scheme in an EU member state when I resign.

Assuming that all of the guarantees in the CEOS are satisfied, what kind of product does the Commission allow me to make the transfer to? Ideally I’d like to put it all into equities with very low fees and start to draw down in twenty years or so at my own pace. I don’t want to be forced to buy an annuity-type product for a payout in 20-odd years as I think this would produce a much lower return and I’m happy to take the risk with equities.

Thanks

Leaving Brussels

Hi! I suggest you stil try to attend one of the seminars organized by PMO about transferring out of pension rights. There are organized regularly.

You can also write to PMO. It’s best to do it through the form on Intranet as then you are identified and find out your precise accumulated capital amount, etc. You can also send an email PMO-TFTOUT-ALLDEP-DEMANDES@ec.europa.eu, if you just want to find out info about a general question.

Last time I attended such a seminar, PMO informed that there is a list of approved 3rd tier pension funds in each EU member state (I wasn’t able to find the list in public sources). You select the fund and its product that appeals to you, and instruct PMO to transfer funds there. You do not always have to transfer to your own country if ther services don’t satisfy you but there were additional rules if you wanted to use a fund in another EU country.

If you find out more, would be great if you could drop me a line so I can add info to this post.

P.S. This is what the form to request the transfer out look like (public source), but you’ll be provided by PMO with this anyway: https://ec.europa.eu/pmo/decl_tft_out_en.pdf

Hi Ben,

Really great post and thread – thanks so much!

I’m a little confused by a few post though (I’m sure it’s just me) so wonder if you can clarify, if you get a chance.

I will shortly be joining an EU agency on a TA contract. The duration is for 5 years but I would hope it will be renewed. I have 3 years of a private pension scheme and a further 11 years of another private pension scheme in an EU member state. I don’t have the current value of these to hand.

My main question is regarding whether I can transfer these into the EU system when I start? Would they be recognised and transferred into “years”? I understand they will be converted into comparable years – ie 100k might be calculated as 3 years 2 months etc etc.

Have you any guidance on how to calculate what the “fund” might be worth in years?

Also, I have a significant number of “state pension” years built up too. Is it possible to transfer this in and forego my state pension for those years in my hole country – i.e from 17 to 38 years of age?

I believe some of these questions have been asked above but can’t quite differentiate between the answers.

Thanks again for all your input here, really really useful

Hi, Max. Congrats on landing the job! Be sure to read about other allowances and enjoy JSIS coverage for you and the family!

I will try to summarize the article.

First, as soon as you’re hired, inquire with HR about PMO (Paymaster’s Office) trainings on the “Transfer-in of pensions”. This will answer your questions in detail. There’s even the option to submit questions and trainers will prepare in-depth replies afterwards.

That’s correct – you don’t get to transfer-in years from national pension systems, but the pension capital which is then “equalized” to your contributions from employment at an EU institution. Unless you’re coming from a very wealthy country, most likely, your many years on the national level will transform to fewer years in the EU institutions pension system.

Unfortunately, only PMO could advise you on how many years you might get when transferring-in.

N.B. Please also read the comment of Anja, 2 November 2021 at 15:11, below.

I hope this was useful!

Dear Ben,

I work currently for EULEX (in Kosovo) and I would like to know if it’s possible to apply for the EU Pension Fund.

Thank you for the useful information. Where can i find the list of the European Commission-approved pension management schemes in all EU member states. I am specifically looking for the pension management schemes in Spain. Thanks a lot for your help.

I remember from a training, that the PMO has this information. If you cannot find this yourself, please call them or write a message (you’ll have to log into an EU system; I couldn’t find a public email): https://ec.europa.eu/pmo/guide/jsis-request-access.html

Hi Ben,

I am nearing retirement and will retire to the UK.

Many years ago I worked 9 years ( duuurgh!!! ) for the EC as a contract agent. I was forced to transfer out my pension. I was given a list of schemes – only 2 were related to the UK and were ‘offshore’. I went with a company in Brussels and received something called ‘Deffered Annuity with Transfer of Benefits’ which will give me an annuity on retirement.

My question is, will this be taxable in Belgium – I don’t see why because the money wasn’t generated in Belgium – but I know nothing of these matters.

First of all, sorry you could not collect the extra 1 year to qualify for the EU pension!

As anything related to pensions is near to arcane magical runes, for this reason I’ll avoid even guessing an answer. It’s also clear that in this case you cannot address PMO, the EU Paymaster’s office.

This totally is a question to your pension fund. Even if they won’t know the answer right away, they are best qualified to provide one as they are located in Belgium and will have access to your case files. Best of luck!

Hi Ben,

Thank you for the information that you post in this web page, and for answering our questions.

According to Article 9 of Annex VIII of the Staff Regulations, “An official leaving the service before reaching pensionable age may request that his retirement pension: (A) be deferred until the first day of the calendar month following that in which he reaches pensionable age; or (B) be paid immediately, provided that he is not less than 58 years of age. In that case, the retirement pension shall be reduced by an amount calculated by reference to the official’s age when he starts to draw his pension”

I just want to clarify something that is not clear in the wording of that article: what happens when the official leaves the service before reaching pensionable age and before he is 58 years of age? Is he then forced to go for option A (deferred pension), or can he still leave the service and when he becomes 58 request option B (early retirement)?

Hi! Sorry for the delayed reply, I unfortunatelly missed your comment/question.

If you have accumulated 10 years in the EU system and have not transferred out your pension capital, you can leave EU institutions and then claim your pension starting from the age of 58.

Dear Ben,

I am a contractual agent with 13 years of work at EU institution and I am very confused on this topic.

On one part, you and PMO.2 pension state that I can leave work at EU Institution also 2 years before early retirement age ( I am 56 years now), and that I that claim my pension once I become 58 years old.

On the other part, HR pension team of my Institution state that I will not be able to claim my pension at the age of 58 if at the time I am not actively working. Please read the HR pension team reply here below:

REPLY from the HR PENSION TEAM

”Dear Nicoletta,

Article 9 of Annex VIII says:

An official leaving the service before reaching retirement age may request that his retirement pension be:

– deferred until the 1st day of the calendar month following that in which he reaches retirement age

– Immediately, if he has reached the age of 58. In this case, the retirement pension is reduced according to the age of the person concerned at the time when his pension starts.

So, if you are not working in a European Institution when you reach the age of 58, you will not be able to take your pension at the age of 58.

You will have a deferred pension at your normal pension age.

The situation will be the same if you benefit from unemployment allowances of the European institutions. ”

I am really puzzle and worried. What happens if I will not find another EU contract until I am 58 years of age?

THank you very much for your reply and support and all the best,

NIcoletta

Hi, as a fired contractor of external company (but work for EC) – do I have some rights to these benefits? I worked (and was allowed to) work remotely from other country and was fired unexpectedly. Do I have any rights? As I know there are much more people like me. Thank You!

Alef, I cannot provide a definitive answer, but from cases similar to yours I’ve gathered that you are not counted as a contractual staff member of any EU institution. Your contractual relationship is only with the company that hired and paid you (even though it was from monies received from the European Commission). I haven’t researched this, but I would look whether maybe there is a labour union that unites employees like you. That might be best placed to provide legal advice to you and also have relevant negotiation and litigation experience.

If you can’t find one, you can always try to approach the labor inspectorate, labor board or an institution of a similar name in the country where your employer was incorporated to receive a consultation about your rights and possibly even further assistance.

Hey there. I am currently ina screening process for an AD7 position in Belgium and I am a Belgian national with 1 daughter. Looking at your explanations, it’s at the same time clear and confusing.

You say that it’s very interesting from a tax perspective as there is no national tax. Approximately it is around 40-45% in Belgium between gross and net salary. Currently I make a bit more in gross per month than the step 1 for AD7 and was trying to compare.

Looking at different taxes you indicate here, it doesn’t seem to be tax free/low tax as it is generally adversited. I see there is a Social security tax (around 12%) , solidarity levy (6%) and EU income tax 8-45%. That brings in total to either 25ish% for lower salaries and (18+45) over 60% tax for higher salaries. Is this how we should understand this ? Because this confuses me as the difference with national taxes is not that different taking into account that I would be granted no expat allowance, no 13 month salary etc. When compared to some private company with a similar position, income and social taxes In Belgium are indeed 40-45%, but largely compensated by the 13 month, company car with fuel card, solid additional group insurance, lunch vouchers and solid group insurance and pension plan, yearly bonuses etc.

So from a pure revenue perspective, even though it is advertised as being tax free or very low taxes while working at EU, globally it’s not that interesting in fact.

Is my reasoning correct ? I may need to consider looking twice before making the move.

Thanks for your reply.

Hi! Apologies for only now replying to you! This is a hobby so I’m at times not able to respond to comments in a timely enough fashion for you and my other readers.

I’ve recently posted articles on the approximate net salaries of the various types of contracts and grades, including AD7, posted here: https://euemployment.eu/administrators-ad7-salary/. The figures should be 90-95% correct, giving you a possibility to compare your income in the Commission vs a private sector employer.

I hope that this article helps you to make decision whether to take the European Commission’s offer.

In case you are considering taking an offer in another EU member state, always remember about the impact of the Correction Coefficient. But this is not a worry if you’re seeking employment in Brussels or Luxembourg.

Dear Ben,

Thank you for all these information that are very useful.

If I was working 15 years in EU institutions as contractual / temporary agent in FG 1 and FG II group with the basic salary always less then AST 1, what would be my pension at the age 66?

1200€ (because my basic salary was always less then AST1 or 1.5x 0,04x AST1, which gives 1800€.

In previous posts i found some calculations for AD 5, AD 10 but not for the contractual/ temporary agents who were working for lower wages.

What if one reaches pension age before accumulating 10 years of service? (E.g. someone who starts working for an eu institution or agency at 58). Such a person would have accumulated pension rights in a national scheme (having worked in their native country before taking up a job for the EU). Could they transfer their national pension rights to the EU scheme? Or would it be wiser for them to keep paying contributions to the national scheme to get a national pension, beause they will not be able to get any kind of EU pension with less than 10 years of service?

Hi Anna,

Did you receive an answer to your question about reaching the pension age before accumulating 10 years of service? In the case of starting working at 58).

Hi, Ana! No, unfortunately I haven’t… I am still interested if anyone has an answer to my question!